Background

Inheritance tax is the only tax in the UK that is supposedly charged on wealth.

If reports from opinion pollsters are to be believed, it is also the most hated tax in the UK[1].

Paradoxically, inheritance tax is also one of the taxes that a person is least likely to pay in the UK. In the tax year 2020/21, which is the last for which reliable statistical data is available, just 3.73 per cent of all estates in the UK were subject to an inheritance tax charge[2].

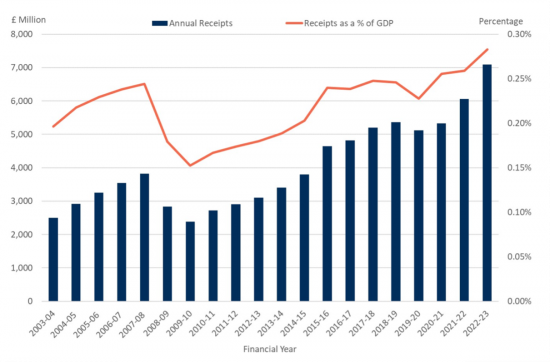

In the last year for which reliable tax collection data for this tax is available (2022/23) the tax yield from inheritance tax was just over £7 billion, which sum amounted to less than one per cent per cent of UK tax receipts as a whole. Both amounts were records, as the following chart indicates[3]:

Annual receipts of inheritance tax and receipts as a proportion of GDP

HM Revenue & Customs has suggested that recent increases in yield are likely to be due to a combination of recent rises in asset values and the government’s decision to maintain the inheritance tax nil rate tax band thresholds at their 2020/21 levels up to and including 2027/2028. Even so, revenue remains modest, overall.

That said, increasing revenues might suggest that concern about this tax is unjustified. There are, however, good reasons to think that inheritance tax is not working as it should.

The problems

Firstly, as a proportion of UK wealth the amount of inheritance tax paid is miniscule. Current estimated UK financial wealth is, according to the Office for National Statistics and in particular its wealth surveys[4] approximately £15,221 billion. The failure of this tax to make any significant inroads into wealth or to tackle wealth inequality suggests that it is poorly designed, inappropriately targeted and highly avoidable by some. That means that the tax is failing to address issues with regard to vertical tax equity and inequality in the UK. It may also be creating horizontal tax inequity.

Secondly, inheritance tax’s treatment of the taxation of former domestic residences, either on death or in the years prior to it, is inequitable. Since property prices vary enormously around the country applying a consistent tax rate of tax on the value of particular asset if above a fixed sum does appear to be particularly unfair. For that reason, a note in the Taxing Wealth Report 2024 series suggests that the inheritance tax charge on former domestic residences should be replaced with a capital gains tax charge on the final disposal of a former domestic residence by a person tax resident within the UK, with certain caveats and conditions attached. The inheritance tax anomaly relating to these assets would be removed as a consequence.

Third, there are significant reasons for concern when this tax appears to be quite effective in imposing charge upon the estates of those with smaller estates primarily made up of lifetime savings and domestic residences but appears to be particularly ineffective when taxing the estates of the wealthiest.

Inheritance tax is in need of reform.

Recommendations

The obvious long-term solution to this problem is to replace inheritance tax with a lifetime gifts receipts tax, which would be substantially more equitable. However, in view of the wide range of other recommendations already been made in the Taxing Wealth Report 2024, a series of more modest recommendations will be made here. They will be:

- To take domestic residences out of the scope of inheritance tax and make them subject to capital gains tax on death or last disposal. This issue is addressed in the capital gains tax section of this report.

- To review inheritance tax business property relief.

- To review inheritance tax agricultural property relief.

- To review inheritance tax charges on personal pension funds.

- To review the use of inheritance tax reliefs on gifts to charities and related issues.

- To review inheritance tax rates and allowances.

Each of these issues is addressed in a separate note within the context of The Taxing Wealth Report 2024.

Detailed proposals

- Abolishing the inheritance tax exemption on some funds retained in pension arrangements at the time of a person’s death might raise £1.3 billion a year.

- Reforming inheritance tax business property relief might raise £3.2 billion of tax a year.

- Reforming inheritance tax agricultural property relief might raise £1.0 billion of tax a year.

- Reforming the rates at which inheritance tax is charged might make the tax considerably more progressive, even if it does not raise revenue.

- Restricting charity tax reliefs to prevent their abuse is important to protect the charity sector from risk.

Future work

Whilst the Taxing Wealth Report 2024 is limiting itself to reforms that might make sense in the short term and which can be adopted in isolation, this does not mean that future work cannot address the significant weaknesses within the structure of this tax, including:

- That the basic logic of a tax on death, charged irrespective of who inherits (charities and spouses apart) makes little sense. A tax on the receipt of gifts would make much more sense and promote greater equality.

- That the rates at which the tax is charged are too inflexible; a progressive scale would make much more sense.

- Arrangements for long-established trusts still mean that some property falls beyond the scope of this tax.

These, however, are issues for further attention in due course and are, as a result, beyond the scope of this current review.

Footnotes

[1] https://www.hl.co.uk/news/articles/archive/britains-most-hated-tax

[2] https://www.gov.uk/government/statistics/inheritance-tax-statistics-commentary/inheritance-tax-statistics-commentary

[3] https://www.gov.uk/government/statistics/hmrc-tax-and-nics-receipts-for-the-uk/hmrc-tax-receipts-and-national-insurance-contributions-for-the-uk-new-annual-bulletin

[4] https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/totalwealthingreatbritain/april2018tomarch2020