Many organisations on the left of UK politics are now calling for wealth taxes. The Taxing Wealth Report 2024 does not do so. It is appropriate to explain why that is the case.

As the Taxing Wealth Report 2024 has shown, because of the disparity between the tax rates applied to income and increases in wealth arising in each year it is possible that an additional capacity to tax of up to £170 billion per annum might be available in the UK. However, just because a potential tax base exists does not mean that it should be taxed. Nor does it mean that the tax base in question must be taxed in only one way.

It is my suggestion that it would not be wise or appropriate to introduce a wealth tax in the UK at this point in time. There are a number of reasons for saying so.

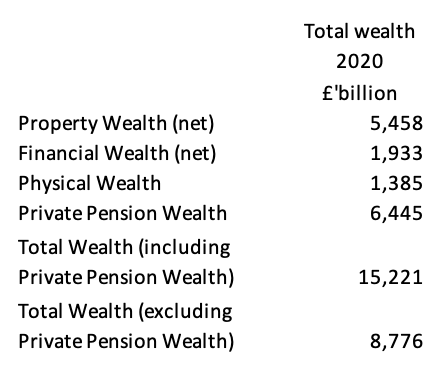

Firstly, whilst it is reported that there was personal wealth exceeding £15 trillion in the UK at the time that the last estimate was prepared in 2020 it is quite clear that a significant part of this might be unavailable as the basis for a wealth tax. The breakdown at that time was as follows:

Much of the UK's property wealth is tied up in private housing and there would be considerable political resistance to imposing a wealth tax charge on people's home, as past evidence has indicated. Whilst it is undeniable that some of that wealth is also second homes, buy-to-let property portfolios, commercial property, and land used for commercial and non-commercial purposes, and all of these might logically be within the basis for a wealth tax, this does not eliminate all the problems of imposing such a charge. There may well, in fact, be considerable difficulty in doing so, because of:

- Establishing who owns a property, since by no means all land and buildings are registered within the UK.

- Valuing these properties when those valuations might be deeply subjective in many cases, and therefore open to considerable (and costly) dispute.

- Establishing a basis for re-evaluation of property values on a recurring basis to ensure that a tax remained relevant. In this context, it should be noted that property valuations for the purposes of Council Tax in England have not been updated since 1992, precisely because of this difficulty.

It would be a brave government that took on these issues. To do so, thinking that the basis for a wealth tax on property could be established within the lifetime of a single parliament, would be wildly optimistic.

Property is not the only area where such difficulties might arise. For example, whilst most physical property would fall outside the scope of a wealth tax because it comprises household effects and things such as cars, there are inevitable exceptions to this rule, including valuable collections, works of art, and so on, all of which could, in theory, be subject to wealth taxation. However, once again, establishing a basis for taxation for such assets and updating it on a regular basis would be exceptionally difficult.

The same problem is to be found with regard to financial wealth. Of the total sum of such wealth noted, it is very unlikely that any government would be willing to impose a wealth tax charge on savings in pension funds. Included in the sum of £1.9 trillion of financial wealth outside such funds is at least £600 billion saved in ISA accounts. It is, again, unlikely that any government would be willing to impose a wealth tax charge on these texts incentivised accounts. This leaves approximately £1.3 trillion of other financial wealth but by no means all of this will be saved in readily marketable assets. Some will, for example, be tied up in the value of private companies and businesses. These are notoriously difficult to value with such valuation exercises often being the subject of protected negotiation and dispute between taxpayers and HM Revenue and Customs, which the imposition of a wealth tax would only make it worse.

Taking all these factors into account it has to, firstly, be concluded that the potential basis for a wealth tax charge is much lower than the total financial wealth of people resident in the UK.

Secondly, it should be apparent that providing an adequate legislative base for such a tax charge would be extremely difficult without creating significant opportunities for loopholes to be exploited.

Thirdly, taking into consideration the need for consultations on all stages of this process, the time required to create such a tax would be considerable.

Fourthly, even if all these processes could be concluded, there would then be a considerable cost to administering this tax because of the inevitable high level of disputes that would arise as to the basis of charge to be made. The fact that those subject to this tax would also, most likely, have the means to engage accountants and lawyers to assist them in pursuing these disputes only increases the likely potential cost of collecting any tax owing.

For all these reasons, it is inappropriate for practical reasons to impose a wealth tax in the UK however appealing such an idea might be when considering the gross inequalities that exist within the country and the apparent disparities in tax paid that we note do arise on a persistent basis.

This does not, however, mean that there are no available taxation solutions to tackling the issues that the Taxing Wealth Report 2024 has noted arise as a consequence of the disparity between the tax rates now paid on income arising during a period and the average increase in wealth of UK households accruing during the same period. What that report suggests in place of a wealth tax are a wide range of reforms to existing taxes payable either on high levels of income, or upon income arising from wealth, or on the enjoyment of certain types of wealth. The breadth of these reforms is potentially quite significant, and include:

- Aligning capital gains tax and income tax rates.

- Reducing the capital gains tax annual allowance.

- Abolishing entrepreneur's relief in capital gains tax.

- Reforming inheritance tax.

- Pensions

- Business property

- Agricultural property

- Charities

- Houses

- Rates

- Reforming rates of income tax.

- Reforming national insurance charges on higher levels of earned income.

- Creating an investment income surcharge on unearned incomes.

- Restricting pension tax reliefs to the basic rate of income tax.

- Abolishing higher rate tax relief on gifts to charities.

- Abolishing the domicile rule.

- Reforming VAT to change tax rates on:

- Private school fees

- Financial advice

- Creating close company corporation tax rules.

- Companies House reform

- Reforming corporation tax admin

- Recreating large and small company corporation tax rates.

- Capping total ISA contributions.

- Council tax reform, including:

- Higher rates of tax for high-value properties

- Additional rates of tax on second and subsequent properties

- Additional taxes on vacant properties.

These reforms are of varying complexity. Some, such as the alignment of income tax and capital gains tax rates, would be easy to implement and have historical precedent. This is also true for investment income surcharges and close company rules for corporation tax, for both of which there are precedents that create significant knowledge bases that would assist the recreation of these charges. In the case of all the potential reforms of this type the creation of new charges should be a relatively straightforward matter, capable of implementation without significant time delays or the creation of substantial taxation disputes. This is the common characteristic to almost all these proposals: they are easy to deliver.

Importantly, however, because of the wide range of options available, it is obvious that not all these changes need to be implemented at the same time, and a rolling programme of reform could, instead, be undertaken. Critically, this suggests that the net outcome of this programme of reform would be significantly more successful than any attempt to impose a single wealth tax.

I offer an analogy by way of explanation. As any golfer knows, setting out to play a round of golf with just one club, whatever it might be, would result in a disastrous score. Golfers take a wide range of clubs because when doing so they have the range of tools necessary to address the wide range of scenarios that they will face whilst completing a game. I suggest that having a single wealth tax would be equivalent to playing a round of golf with, for example, a putter. Having the range of tax reforms proposed in the Taxing Wealth Report 2024 might instead be the equivalent to setting off with fourteen clubs in the golfer's bag, which considerably increases the chance of achieving a good score. So it is with taxation. Having a wide ranges of taxes imposed at relatively low rates on relatively easy to identify tax bases is likely to produce an overall taxation yield greater than a single tax on a peculiar tax base might ever achieve. It is on the basis of this logic that the Taxing Wealth Report 2024 has been written. Reforming existing taxes can achieve so much more than a wealth tax might.

A summary of the proposals made in the Taxing Wealth Report 2024 is available here.