I have this morning published the next in my series of proposals that will together make up the Taxing Wealth Report 2024.

In this note, I suggest that a radical reform of the administration of corporation tax in the UK is required. When only one-third of companies in the UK pay tax, millions do not submit corporation tax returns, and hundreds of thousands disappear each year without questions being asked, there is something seriously wrong with the way in which this tax is being administered at present.

I suggest that on the basis of the radical reforms that I propose that at least £6 billion of additional tax revenue might be raised a year, but it is likely that this is a serious underestimate because these measures should also significantly reduce the scale of fraud on the government each year.

The summary to this note says:

Brief Summary

This note proposes that:

- The administration of corporation tax by HM Revenue & Customs needs to be substantially reformed if the abuse of limited liability companies to illicitly accumulate untaxed wealth is to be prevented.

- The current lax regime for the requesting of a corporation tax return by HM Revenue & Customs should be replaced by a mandatory obligation that a company file such a return with attached accounts each year.

- That the directors and principal shareholders of a company should be required to prove their identities and current address to HM Revenue & Customs and Companies House annually.

- That the directors and principal shareholders of a company failing to supply a corporation tax return should be liable for the penalties due as a result of that failure. The latest available research on this issue suggests that 99 per cent of those penalties are unpaid at present.

- The directors and principal shareholders of a company should be liable for any tax of any sort owing by it if unpaid by the company itself unless they can demonstrate a clear commercial reason for which they were not responsible that explains the inability to pay.

- Any banker, lawyer, accountant or other person in the financial services industry acting on behalf of a company who is required by law to prove the identity of that company's directors and principal shareholders shall be required by law to provide an annual declaration to HM Revenue & Customs and Companies House confirming those identities, or a statement as to why they are unable to do so.

- Any bankers and accountants supplying services to or acting on behalf of any company in a year should be required by law to supply details of the total payments received in that company's bank accounts during each of its financial years within nine months of the end of that period so that in the absence of a corporation tax HM Revenue & Customs can raise an estimated assessment of those taxes that they think it might owe for which the directors and principal shareholders shall be liable unless they can disprove that claim.

- That these proposals should considerably reduce the amount of tax evasion in the UK, which HM Revenue & Customs estimates to be £19 billion per annum, but which might be very much higher, most of which will be undertaken through limited liability companies. A revenue estimate of £6 billion is estimated to arise as a result of these changes.

- These proposals might also considerably reduce the scale of fraud perpetrated on the government each year, which is estimated to be between £33 billion and £58 billion per annum excluding Covid related issues. No revenue estimate is made for the likely gain resulting.

The illicit accumulation of wealth in the UK that contributes significantly to inequality might be reduced as a consequence of these changes.

Discussion

This is one of the longer notes that will make up the Taxing Wealth Report 2024. This is also a complex note which should, however, reward those who take the time to read it. A related note on the need for reform to the operations of Companies House will be published soon.

The core suggestion that this note makes is that HM Revenue & Customs does not know which companies are trading in the UK and appears to be indifferent to its ignorance on this issue and the tax consequences that flow from it.

The suggestion is made that limited liability companies (and related entities) are being seriously abused to assist the evasion of tax in the UK.

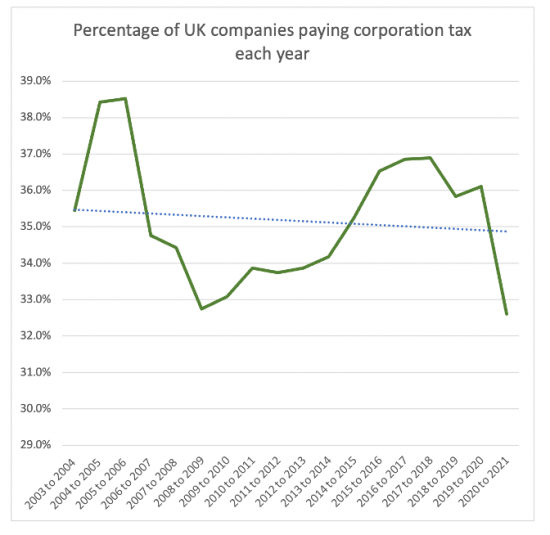

Only one in three companies in the UK pay tax and the trend is downward:

As a result, a number of recommendations are made that might appear onerous at first sight but which are, in fact, no more than what is now demanded from tax haven jurisdictions under Organisation for Economic Cooperation and Development automatic information exchange rules. If we can impose such requirements on other places, it seems to be absurd that we cannot do so domestically when the scale of tax losses resulting within the UK economy is likely to be much higher than that arising from the abuse of tax havens.

There would, no doubt, be significant objection to the proposals made, including removing the advantage of limited liability from those directors and principal shareholders (those owning more than ten per cent of a company) who use the ready availability of limited liability companies in the UK to abuse markets and unjustly enrich themselves. Those objections should, however, be ignored. Limited liability is a privilege and not a right, and it is one that cannot be abused. If regulation can be imposed on drivers because they create a risk to society by using their cars, regulation that will cost much less a year for a company to comply with in most cases can also be imposed on all corporate entities registered in the UK to prevent the risk that they create to society.

The estimate of tax yield resulting from this proposal is very likely understated, but since the scale of tax fraud in the UK is unknown because we do not have proper tax gap appraisals, this is something that has to be accepted for now.

Cumulative value of recommendations made

The recommendations now made as part of the Taxing Wealth Report 2024 would, taking this latest proposal into account, raise total additional tax revenues of approximately £76.3 billion per annum.